To be fair, accidents happen every single day, and in the United States, more than five million accidents occur each year. In fact, chances are your insurance will one day come in handy, and so will GAP insurance, a little known additional piece of insurance that many people don’t understand.

What is GAP insurance? How does it work, and how could it benefit you? Keep reading as Car Bibles details the answers to all your burning questions and fills you in about GAP insurance.

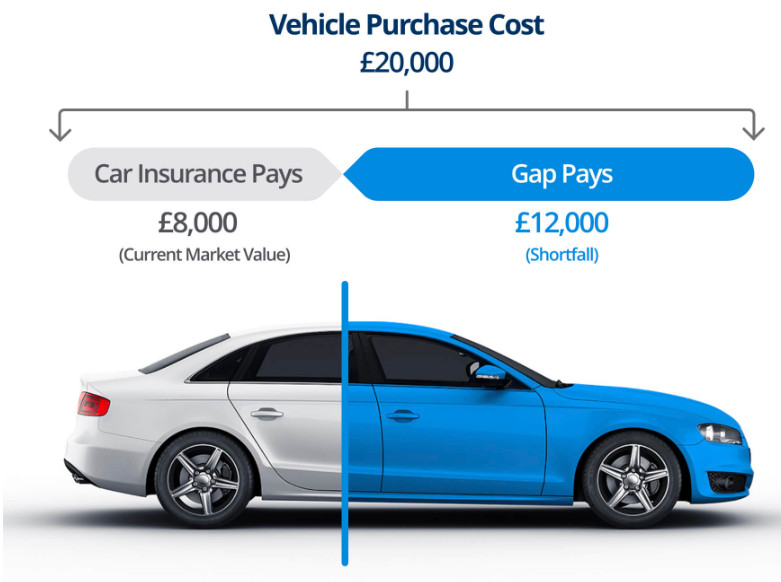

What Is GAP Insurance?

GAP stands for guaranteed asset protection. It covers the difference between the current depreciated value of your car and how much you still owe on it. For example, if you get into an accident and the car’s depreciated value ($22,000) is less than you still owe ($27,000), GAP insurance will help you pay off the residual amount you owe ($5,000), so you’re not on the hook for a car that’s sitting in a scrapyard.

How Does GAP Insurance Work?

GAP insurance works like most other insurance plans. To be insured, you pay a specific amount of money in intervals of one or six months. The plan you choose then covers you if/when an accident occurs and you’re still under water with your car payments. It’s usually an optional policy extra when you’re shopping for car insurance.

What Are the Benefits?

The major benefit to GAP insurance is that you’re covered if you get into an accident and you still owe a bunch toward your car’s purchase price. If you didn’t have GAP insurance and you still owed money at the time of the accident, you’re still on the hook for that money. So, if it’s put to use, it will theoretically save you money.

What Are the Cons?

The biggest and most crucial downside to GAP insurance is that it increases your insurance bill. It’s up to you to decide whether or not you should risk driving without this type of insurance.

Do I Really Need GAP Insurance?

You don’t if your car payment is enough to cover for depreciation or if you have a car that’s actually appreciating in value. That’s not the case for most, however, as only a few select cars actually appreciate and payments that cover depreciation are often quite large.

If you’ve gone for a 72-84-month loan and only put down a few thousand dollars, GAP insurance might be right for you. You’ll have to make that decision for yourself — I’m not your mother or your financial adviser. I don’t know your individual situation, your finances, or the vehicle you purchased. What I’d tell you is to do your research on your car’s projected depreciation.

Scroll through KBB and look at used values of the same vehicle you’re in the market for, how much you’re willing to drop on your down payment, and determine how long of a loan you’re comfortable taking. The shorter the term, the more expensive your monthly payments will be, but the lesser the risk that your payments won’t align with your car’s depreciation.

What’s the Best Way to Get GAP Insurance?

Talk to your current insurance company. It should be a fairly painless process. You’ll likely need all the regular expected documents like your license, your current insurance plan, your car’s financial documents, your car’s VIN, and the title.

FAQs About GAP Insurance

Car Bibles answers your burning questions.

Q. How much does GAP insurance cost?

A. That depends on your individual situation, as there’s no single blanket cost per policyholder. You’ll have to contact your insurance company to find out more. However, the average cost in the U.S. is between $20 and $40 per year.

Q. Is GAP insurance worth it?

A. It can be. If your financial situation necessitates a vehicle (whose doesn’t?), and you agree to pay over a longer term or a higher price due to vehicle shortages and dwindling dealership stock, then GAP insurance could insulate you in the case of an accident.

Q. Do you need GAP insurance if you have full coverage?

A. You betcha. Full coverage doesn’t include GAP insurance, despite its name.

Learn More From This Video on GAP Insurance

The Car Bibles editors understand that not everyone is a text-based learner. For those kinesthetic learners, we have your back with a video discussing buying salvage cars.

Disclosure: AZCarBlog.com is also a participant in the Amazon Services LLC Associate Programs, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Pages on this site may include affiliate links to Amazon and its affiliate sites on which the owner of this website will make a referral commission.

Originally posted 2023-12-13 13:50:18.